You earn a decent income. You don't think you're spending recklessly. And yet every month, you check your account and wonder: *where did it all go?*

You're not imagining it. Here's what the data actually shows.

Want to see where your own money actually goes? Try Spendalyst free for 14 days →

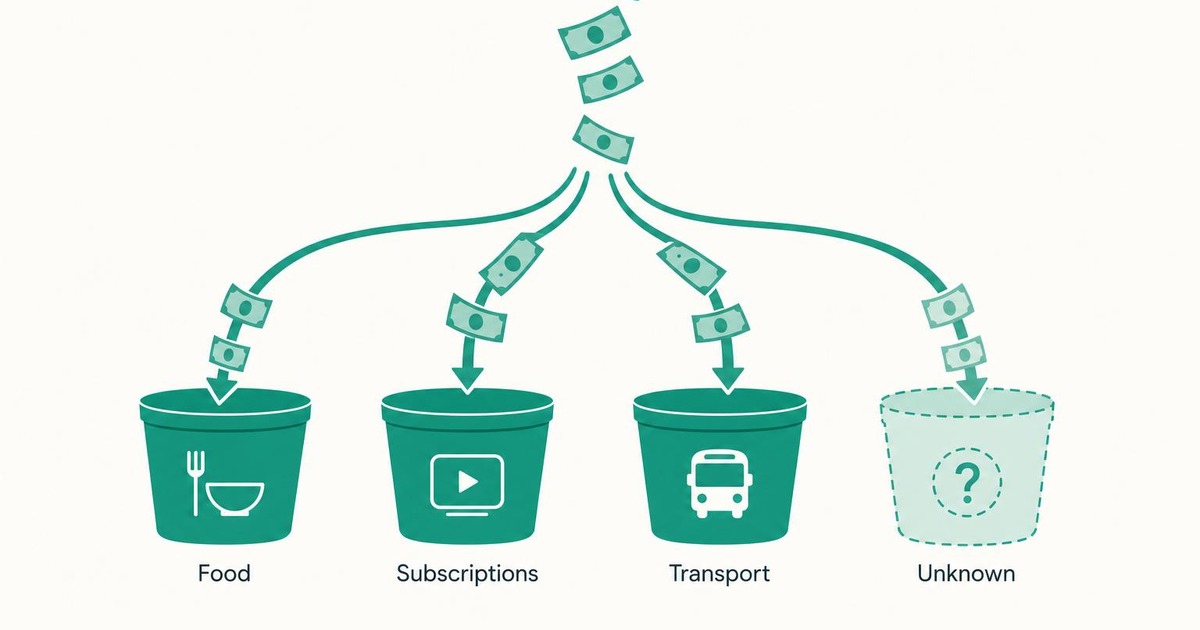

Where Most People's Money Actually Goes

Research on spending patterns consistently shows the same surprises:

Food is the biggest shock. Most people dramatically underestimate what they spend on food — because they're mentally separating "groceries" from "delivery" from "restaurants" from "coffee." Combined, food often runs $500–$900/month for a single person without them realizing it.

Subscriptions are invisible. The average American pays for 4–6 more subscriptions than they remember having. These auto-renew, they're small enough to ignore individually, and they add up to $80–$200/month.

Convenience spending is high and hard to see. Ubers instead of driving. Delivery instead of cooking. One-click online purchases. Each one feels minor. The category total rarely does.

Irregular expenses feel like emergencies. Car maintenance, doctor visits, holiday gifts, annual renewals — these aren't surprises, but without visibility, they feel like ones.

Why Traditional Tracking Doesn't Work

Most people try one of two things:

Both put the burden on *you* — to predict, to categorize, to stay consistent. That's why most people quit.

A Better Way: Let the Data Show You

Instead of trying to plan your spending in advance, start by *seeing what already happened*.

Connect your bank to Spendalyst and within minutes you'll see:

No setup. No categories to assign. No budget to maintain.

Just an honest picture of where your money went — and enough context to decide what, if anything, you want to change.

[See where your money is going →](https://app.spendalyst.com)

The Goal Isn't Perfection

You don't need to cut everything. You don't need a perfect budget. You just need enough clarity to make intentional choices.

Most people who start using Spendalyst don't dramatically change their lifestyle — they just eliminate one or two things they weren't even enjoying. That's usually enough to feel financially stable instead of financially stressed.